Ying Huang, Juan Hu, and Jing Chen

School of Foreign Languages, Wuhan City Polytechnic, Wuhan 430064, China

Received: March 2, 2026

Accepted: April 1, 2026

Publication Date: June 1, 2026

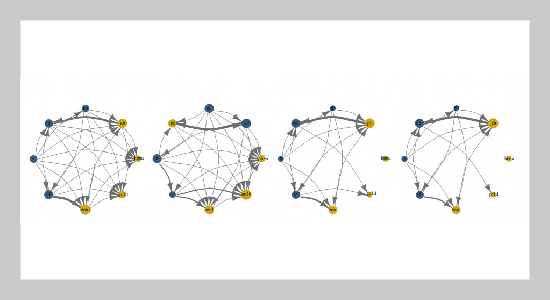

Spillover Networks in Time, High-, Medium- and Low- Frequency Domains.

Copyright The Author(s). This is an open access article distributed under the terms of the Creative Commons Attribution License (CC BY 4.0), which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are cited.

Download Citation: BibTeX | http://dx.doi.org/10.6180/jase.202609_32.064

The diverse roles of green financial sub-markets and their dynamic risk spillovers to the carbon market are important to explain the systemic risks of Chinese low-carbon transition. We employ a Time-Varying Parameter Vector Autoregression (TVP-VAR) model with time-frequency decomposition to explore the connections in China’s carbon-green finance system between January 2016 and January 2025. The findings indicate major bidirectional asymmetric spillovers, with the greater impacts of green financial markets on the carbon market. Particularly, functional heterogeneity is strong across the green financial sub-markets. Green equity markets serve as persistent risk transmitters whereas green bonds are transitional, changing from short-term risk transmitters to long-term stabilizers. The carbon market is regularly a net risk recipient due to its policy-driven nature. On the dynamic features, cross-market linkages are highly time-frequency asymmetries, dominated by short-term speculative spillovers and amplified by extreme events and policy shifts. Moreover, there are clear temporal heterogeneities in the risk transmission paths, where short-run flows are sentiment-led and long-run are fundamentals-led. Understanding these dynamics is crucial for both policy-makers and investors in dealing with systemic climate-finance risks.

Keywords: carbon market; green financial market; dynamic risk spillovers; TVP-VAR-DY; TVP-VAR-BK; Computer network

- [1] N. Koch, (2014) “Dynamic linkages among carbon, energy and financial markets: a smooth transition approach” Applied Economics 46(7): 715–729. DOI: 10.1080/00036846.2013.854301.

- [2] X. Tan, K. Sirichand, A. Vivian, and X. Wang, (2020) “How connected is the carbon market to energy and financial markets? A systematic analysis of spillovers and dynamics” Energy Economics 90: 104870. DOI: 10.1016/j.eneco.2020.104870.

- [3] J. Jin, L. Han, L. Wu, and H. Zeng, (2020) “The hedging effect of green bonds on carbon market risk” International Review of Financial Analysis 71: 101509. DOI: 10.1016/j.irfa.2020.101509.

- [4] W. Hanif, J. A. Hernandez, W. Mensi, S. H. Kang, G. S. Uddin, and S.-M. Yoon, (2021) “Nonlinear dependence and connectedness between clean/renewable energy sector equity and European emission allowance prices” Energy Economics 101: 105409. DOI: 10.1016/j.eneco.2021.105409.

- [5] Y. Zhang and M. Umair, (2023) “Examining the interconnectedness of green finance: an analysis of dynamic spillover effects among green bonds, renewable energy, and carbon markets” Environmental Science and Pollution Research 30(3): 77605–77621. DOI: 10.1007/s11356-023-27870-w.

- [6] I. Chatziantoniou, E. J. A. Abakah, D. Gabauer, and A. K. Tiwari, (2022) “Quantile time–frequency price connectedness between green bond, green equity, sustainable investments and clean energy markets” Journal of Cleaner Production 361: 132088. DOI: 10.1016/j.jclepro.2022.132088.

- [7] R. Wu and Z. Qin, (2024) “Asymmetric volatility spillovers among new energy, ESG, green bond and carbon markets” Energy 292: 130504. DOI: 10.1016/j.energy.2024.130504.

- [8] Z. Huang, X. Ding, and Y. Wang, (2026) “Risk spillover and network connectedness analysis of green financial and related financial markets: evidence from China” Humanities and Social Sciences Communications 13(1): 344. DOI: 10.1057/s41599-026-06706-1.

- [9] J. Deng, Y. Zheng, and X. Gu et al., (2023) “Research on the Spillover Effects between China’s Carbon Market and Green Finance Market” Financial Theory & Practice 44(7): 48–59. DOI: 10.3969/j.issn.1003-4625.2023.07.005.

- [10] L. Yan and W. Han, (2025) “The complexity of connection between green bonds and carbon markets: New evidence from China” Finance Research Letters 84: 107790. DOI: 10.1016/j.frl.2025.107790.

- [11] T. Hui, Z. Wang, and Z. He, (2025) “Research on the Spillover Effects of China’s Carbon Market and Green Finance Market” Soft Science 39(6): 17. DOI: 10.13956/j.ss.1001-8409.2025.06.17.

- [12] S. Qi, L. Pang, X. Li, and L. Huang, (2025) “The dynamic connectedness in the “carbon–energy–green finance” system: The role of climate policy uncertainty and artificial intelligence” Energy Economics 143: 108241. DOI: 10.1016/j.eneco.2025.108241.

- [13] X. Wang and M. Liu, (2025) “Research on Risk Spillover Effects Among Carbon–Energy–Green Finance Markets” Distributed Energy 10(4): 24–34. DOI: 10.16513/j.2096-2185.DE.25100017.

- [14] W. Jiang, L. Dong, and X. Liu, (2023) “How does COVID-19 affect the spillover effects of green finance, carbon markets, and renewable/non-renewable energy markets? Evidence from China” Energy 281: 128351. DOI: 10.1016/j.energy.2023.128351.

- [15] S. Agarwal and P. Padhi, (2025) “Connectedness among green, brown, technology, and carbon markets: Insights from time-varying models” International Review of Economics & Finance: 104762. DOI: 10.1016/j.iref.2025.104762.

- [16] F. X. Diebold and K. Yılmaz, (2012) “Better to give than to receive: Predictive directional measurement of volatility spillovers” International Journal of Forecasting 28(1): 57–66. DOI: 10.1016/j.ijforecast.2011.02.006.

- [17] N. Antonakakis, I. Chatziantoniou, and D. Gabauer, (2020) “Refined measures of dynamic connectedness based on time-varying parameter vector autoregressions” Journal of Risk and Financial Management 13(4): 84. DOI: 10.3390/jrfm13040084.

- [18] I. Chatziantoniou, D. Gabauer, and R. Gupta, (2023) “Integration and risk transmission in the market for crude oil: New evidence from a time-varying parameter frequency connectedness approach” Resources Policy 84: 103729. DOI: 10.1016/j.resourpol.2023.103729.

- [19] J. Baruník and T. Křehlík, (2018) “Measuring the frequency dynamics of financial connectedness and systemic risk” Journal of Financial Econometrics 16(2): 271–296. DOI: 10.1093/jjfinec/nby001.

- [20] F. X. Diebold and K. Yılmaz, (2014) “On the network topology of variance decompositions: Measuring the connectedness of financial firms” Journal of Econometrics 182(1): 119–134. DOI: 10.1016/j.jeconom.2014.04.012.

- [21] W. Mensi, X. V. Vo, H.-U. Ko, and S. H. Kang, (2023) “Frequency spillovers between green bonds, global factors and stock market before and during COVID-19 crisis” Economic Analysis and Policy 77: 558–580. DOI: 10.1016/j.eap.2022.12.010.

- [22] Y. Wang, X. Zhao, and J. Shang, (2025) “Dynamic risk spillover in green financial markets: A wavelet frequency analysis from China” Energy Economics 143: 108301. DOI: 10.1016/j.eneco.2025.108301.

- [23] M. Zhao and H. Park, (2024) “Quantile time-frequency spillovers among green bonds, cryptocurrencies, and conventional financial markets” International Review of Financial Analysis 93: 103198. DOI: 10.1016/j.irfa.2024.103198.

- [24] J. Baruník and M. Ellington, (2024) “Persistence in financial connectedness and systemic risk” European Journal of Operational Research 314(1): 393–407. DOI: 10.1016/j.ejor.2023.11.023.

- [25] X. Jin, (2025) “Extreme Risk Connectedness and its Determinants Between Carbon, Green Finance and Energy Markets” Asia-Pacific Financial Markets: 1–34. DOI: 10.1007/s10690-025-09536-4.

- [26] P. Maneejuk, W. Huang, and W. Yamaka, (2025) “Asymmetric volatility spillover effects from energy, agriculture, green bond, and financial market uncertainty on carbon market during major market crisis” Energy Economics 145: 108430. DOI: 10.1016/j.eneco.2025.108430.

- [27] Q. Li, (2025) “Financial stress and idiosyncratic risk spillovers in global carbon–energy–green finance markets” Finance Research Letters: 109362. DOI: 10.1016/j.frl.2025.109362.