Experimental Training Teaching Center, Yanshan college Shandong University of Finance and Economics, Jinan, Shandong 271199, China

Received: November 26, 2025

Accepted: January 31, 2026

Publication Date: March 15, 2026

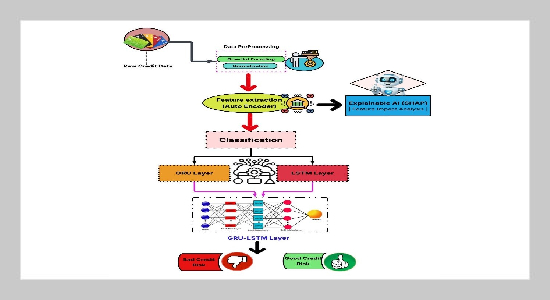

Credit Risk Assessment System Proposed Methodology Architecture

Copyright The Author(s). This is an open access article distributed under the terms of the Creative Commons Attribution License (CC BY 4.0), which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are cited.

Download Citation: BibTeX | https://doi.org/10.6180/jase.202608_31.036

This research presents an explainable deep learning framework for credit risk assessment that integrates an unsupervised autoencoder with a GRU–LSTM hybrid model for sequential data classification. Traditional credit scoring systems face several challenges, including difficulty in capturing complex borrower behavioral patterns, methodological limitations, and a lack of explainability, which reduces their suitability for decision-making in dynamic financial environments. The proposed framework employs an autoencoder to preprocess data by reducing dimensionality and noise, while the GRU–LSTM architecture captures both short- and long-term dependencies in borrower behavior. The autoencoder performs dimensionality reduction by compressing high-dimensional input features into a smaller latent representation through an encoder network trained to reconstruct the original data with minimal information loss. This process removes redundant and noisy attributes while preserving the most informative patterns required for accurate credit risk classification. To support interpretable credit risk evaluation, SHapley Additive exPlanations (SHAP) is used to provide both local and global feature importance explanations. By quantifying the contribution of each input feature to individual predictions, the explainability component supports transparent credit decisions and enables financial institutions to justify automated outcomes within regulatory and auditing workflows. The framework was implemented using Python and evaluated on the German Credit dataset after preprocessing with one-hot encoding and Min–Max normalization. Experimental results demonstrate strong performance, achieving an accuracy of 99.12%, precision of 98.82%, recall of 98.78%, and an F1-score of 98.851. These findings indicate that the framework provides an accurate, explainable, and real-time approach to credit risk assessment in institutional financial settings.

Keywords: Credit risk assessment; Deep learning; Autoencoder; GRU-LSTM; Explainable AI; SHAP; Feature extraction;

Classification

- [1] N. Mansour, (2023) “Green Technology Innovation and Financial Services System: Evidence from China” Businesses 3(1): 1. DOI: 10.3390/businesses3010008.

- [2] X. Zhang et al., (2025) “Data-Driven Loan Default Prediction: A Machine Learning Approach for Enhancing Business Process Management” Systems 13(7): 581. DOI: 10.3390/systems13070581.

- [3] H. Tajik, G. Talebnia, H. R. Vakilifard, and F. Ahmadi, (2024) “Machine learning support to provide an intelligent credit risk model for banks’ real customers” International Journal of Nonlinear Analysis and Applications 15(4): 23–42. DOI: 10.22075/ijnaa.2022.28382.3874.

- [4] S. R. Challa, (2023) “Artificial Intelligence and Big Data in Finance: Enhancing Investment Strategies and Client Insights in Wealth Management” International Journal of Scientific Research 12(12): 2230–2246. DOI: 10.21275/sr231215165201.

- [5] C. Guan, H. Suryanto, A. Mahidadia, M. Bain, and P. Compton, (2023) “Responsible Credit Risk Assessment with Machine Learning and Knowledge Acquisition” Human-Centered Intelligent Systems 3(3): 232–243. DOI: 10.1007/s44230-023-00035-1.

- [6] Á. Beade, M. Rodríguez, and J. Santos, (2024) “Business failure prediction models with high and stable predictive power over time using genetic programming” Operations Research International Journal 24(3): 52. DOI: 10.1007/s12351-024-00852-7.

- [7] C. N. Nwafor, O. Nwafor, and S. Brahma, (2024) “Enhancing transparency and fairness in automated credit decisions: an explainable novel hybrid machine learning approach” Scientific Reports 14(1): 25174. DOI: 10.1038/s41598-024-75026-8.

- [8] M. Nagashima-Hayashi et al., (2022) “Gender-Based Violence in the Asia-Pacific Region during COVID-19: A Hidden Pandemic behind Closed Doors” International Journal of Environmental Research and Public Health 19(4): 2239. DOI: 10.3390/ijerph19042239.

- [9] S. Gholampour, (2024) “Impact of Nature of Medical Data on Machine and Deep Learning for Imbalanced Datasets: Clinical Validity of SMOTE Is Questionable” Machine Learning and Knowledge Extraction 6(2): 39. DOI: 10.3390/make6020039.

- [10] Y. Bao, G. Hilary, and B. Ke. “Artificial Intelligence and Fraud Detection”. In: Innovative Technology at the Interface of Finance and Operations. Springer, 2022, 223–247. DOI: 10.1007/978-3-030-75729-8_8.

- [11] D. Slack, S. Krishna, H. Lakkaraju, and S. Singh, (2023) “Explaining machine learning models with interactive natural language conversations using TalkToModel” Nature Machine Intelligence 5(8): 873–883. DOI: 10.1038/s42256-023-00692-8.

- [12] T. Berhane, T. Melese, A. Walelign, and A. Mohammed, (2023) “A Hybrid Convolutional Neural Network and Support Vector Machine-Based Credit Card Fraud Detection Model” Mathematical Problems in Engineering 2023: 8134627. DOI: 10.1155/2023/8134627.

- [13] D. Halvoník and J. Kapusta, (2024) “Large Language Models and Rule-Based Approaches in Domain-Specific Communication” IEEE Access 12: 107046–107058. DOI: 10.1109/ACCESS.2024.3436902.

- [14] Z. Amiri et al., (2023) “The Personal Health Applications of Machine Learning Techniques in the Internet of Behaviors” Sustainability 15(16): 12406. DOI: 10.3390/su151612406.

- [15] M. Kinney, M. Anastasiadou, M. Naranjo-Zolotov, and V. Santos, (2024) “Expectation management in AI: A framework for understanding stakeholder trust and acceptance of artificial intelligence systems” Heliyon 10(7): e28562. DOI: 10.1016/j.heliyon.2024.e28562.

- [16] C. N. Nwafor, O. Nwafor, and S. Brahma, (2024) “Enhancing transparency and fairness in automated credit decisions: an explainable novel hybrid machine learning approach” Scientific Reports 14(1): 25174. DOI: 10.1038/s41598-024-75026-8.

- [17] L. Liu, (2022) “A Self-Learning BP Neural Network Assessment Algorithm for Credit Risk of Commercial Bank” Wireless Communications and Mobile Computing 2022: 9650934. DOI: 10.1155/2022/9650934.

- [18] N. Biswas, A. S. Mondal, A. Kusumastuti, S. Saha, and K. C. Mondal, (2025) “Automated credit assessment framework using ETL process and machine learning” Innovations in Systems and Software Engineering 21(1): 257–270. DOI: 10.1007/s11334-022-00522-x.

- [19] Z. Yu, (2023) “Prediction of Credit Card Loan Risk Based on Multilayer Perceptron Neural Network Model” BCPBM 38: 126–134. DOI: 10.54691/bcpbm.v38i.3679.

- [20] J. Hu, H. Wang, and X. Lu, (2023) “Research on Credit Risk Assessment Model of Enterprises’ Unpaid Electricity Charge Based on Machine Learning Method” SHS Web of Conferences 170: 03023. DOI: 10.1051/shsconf/202317003023.

- [21] T. A. O. Odejide, (2024) “Theoretical frameworks in AI for credit risk assessment: Towards banking efficiency and accuracy” International Journal of Scientific Research Updates 7(1): 092–102. DOI: 10.53430/ijsru.2024.7.1.0030.

- [22] S. B. Coşkun and M. Turanli, (2023) “Credit risk analysis using boosting methods” Journal of Applied Mathematics, Statistics and Informatics 19(1): 5–18. DOI: 10.2478/jamsi-2023-0001.

- [23] C. Rao, Y. Liu, and M. Goh, (2023) “Credit risk assessment mechanism of personal auto loan based on PSO-XGBoost Model” Complex & Intelligent Systems 9(2): 1391–1414. DOI: 10.1007/s40747-022-00854-y.

- [24] S. Luo, M. Xing, and J. Zhao, (2022) “Construction of Artificial Intelligence Application Model for Supply Chain Financial Risk Assessment” Scientific Programming 2022: 4194576. DOI: 10.1155/2022/4194576.

- [25] Y. Bai and D. Zha, (2022) “Commercial Bank Credit Grading Model Using Genetic Optimization Neural Network and Cluster Analysis” Computational Intelligence and Neuroscience 2022: 4796075. DOI: 10.1155/2022/4796075.

- [26] G. F. Bone-Winkel and F. Reichenbach, (2024) “Improving credit risk assessment in P2P lending with explainable machine learning survival analysis” Digital Finance 6(3): 501–542. DOI: 10.1007/s42521-024-00114-3.

- [27] M. R. Machado, D. T. Chen, and J. R. Osterrieder, (2025) “An analytical approach to credit risk assessment using machine learning models” Decision Analytics Journal 16: 100605. DOI: 10.1016 / j. dajour. 2025 . 100605.

- [28] N. A. de Oliveira and L. F. C. Basso, (2025) “Advancing Credit Rating Prediction: The Role of Machine Learning in Corporate Credit Rating Assessment” Risks 13(6): 116. DOI: 10.3390/risks13060116.

- [29] M. Sarıkoç and M. Celik, (2025) “PCA-ICA-LSTM: A Hybrid Deep Learning Model Based on Dimension Reduction Methods to Predict S&P 500 Index Price” Computational Economics 65(4): 2249–2315. DOI: 10.1007/s10614-024-10629-x.

- [30] C. Wang and H. Yu, (2025) “Intelligent Assessment of Personal Credit Risk Based on Machine Learning” Systems 13(2): 112. DOI: 10.3390/systems13020112.

- [31] K. Dwi Hartomo, C. Arthur, and Y. Nataliani, (2025) “A Novel Weighted Loss TabTransformer Integrating Explainable AI for Imbalanced Credit Risk Datasets” IEEE Access 13: 31045–31056. DOI: 10.1109 / ACCESS.2025. 3541878.

- [32] Credit Risk Evaluation. Kaggle Notebook. Accessed July 21, 2025. 2025.